Do You Know What an IUL Policy Is, or How It Works?

As an agent, you may already have an understanding of Index Universal Life policies or how they work. But do you know how to explain an IUL policy in a simplified way to your clients? Look no further! The key to bringing your clients up to speed in the most simple way is here!

IUL Policy Basics

Indexed universal life policies fall into the category of permanent life insurance. These policies offer death benefit protection when death happens. Additionally, the premium payments have the ability to earn interest to build cash value on the policy. The key component setting IUL policies apart from other permanent insurance policies is the way the interest credits to the policy. More than offering a set traditional declared interest rate, indexed universal life has the ability to earn interest linked to the rise of a chosen index in the stock market over a specific period of time with the policy. A key point of this is that the additional earned interest is earned based on the rise. This means if the index becomes negative, the policy will not lose its value.

Try this IUL Policy Breakdown with your Clients:

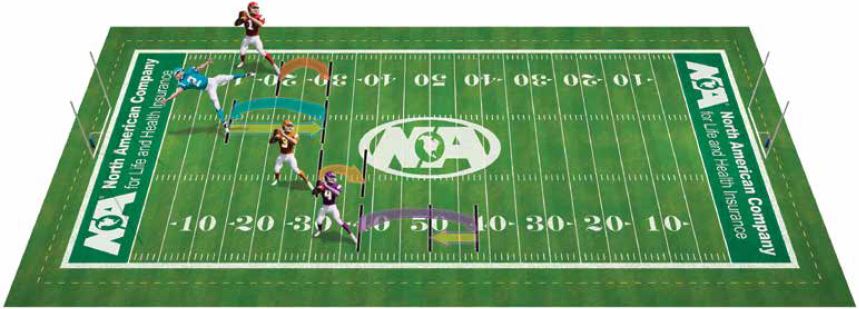

RULES OF THE GAME:

If the Index Account were a game of football and the football team was an Index Selection in a life insurance policy, here’s how the rules would change: Perpetual first down. No negative yards. Gain up to a maximum of 12 yards per play.

Take a look at what happens with these “new rules.”

THE PLAY-BY-PLAY:

Pick your favorite quarterback. His team has the ball and is starting out on the 20-yard line.

Play 1 (red): Your quarterback throws for a 10-yard gain! The ball is on the 30-yard line.

Play 2 (blue): Your quarterback is sacked at the 12-yard line for an 18-yard loss. However, we’ve changed the rules so that instead of losing yards the ball is on the 30-yard line where the play began, and it’s still first down.

Play 3 (orange): Your quarterback throws for an 8-yard gain. The ball is on the 38-yard line, and it’s still first down.

Play 4 (purple): Your quarterback throws for a 19-yard gain. The 12-yard maximum kicks in; as a result, your team has to “give back” seven of the yards. The net result is a gain of 12 yards, and the ball is on the 50-yard line.

GAME SUMMARY:

Under normal rules, the team would have gained a total of 19 yards (gains of 10, 8, and 19 with a loss of 18 yards) and the ball would be on the 39-yard line. However, with the new rules, the team gained 30 yards and the ball is at the 50-yard line. As a result, an extra 11 yards downfield!

WHAT DOES THIS MEAN FOR YOUR CLIENT?

Imagine if the football team was an Index Selection in a life insurance policy. The maximum 12-yard rule represents the cap rate, and the fact you never lose yards is similar to a no-downside risk. Each play is a year, and the yardage gains are locked in interest crediting!

Agents

We hope that this information on an IUL policy is useful to you.

Empower Brokerage is dedicated to helping you make informed decisions about your health and finances. Whether it’s through webinar training, one-on-one calls, seminars, or marketing plans, we want you to be successful!

Give us a call at 888-539-1633 or leave a comment below if you have any questions.

Quick links: